Par dérogation à l'article 4.25 des conditions générales, sont garanties les conséquences pécuniaires de la responsabilité civile que l'assuré peut encourir en raison des dommages matériels – ainsi que les dommages immatériels qui en sont la conséquence – causés aux biens mobiliers qui font l'objet de la prestation de l'assuré, qu'ils soient ou non des biens confiés au sens de la définition figurant aux conditions générales ainsi que les biens empruntés pour sa réalisation.

La garantie est étendue en cas de vol, perte ou disparition des clefs confiées à l'assuré, à ses préposés ou à ses sous-traitants par ses clients dans le cadre du contrat de prestation aux frais strictement nécessaires à la réfection des clefs, canons et serrures.

Sans préjudice des exclusions prévues par ailleurs, demeurent exclus de la garantie :

- Dommages aux biens remis dans le cadre d'un contrat de dépôt rémunéré ou remis pour vente ou location

- Dommages aux biens loués ou prêtés à titre onéreux ou faisant l'objet d'un crédit-bail

- Dommages survenus au cours d'un transport, sauf transport accessoire non professionnel

- Dommages aux espèces, objets de valeur (titres, bijoux, pierreries, perles, métaux précieux, œuvres d'art)

- Objets fragiles : verreries, porcelaines, terres cuites, plâtres, statues, céramiques, miroirs

- Objets déjà en mauvais état avant le sinistre

- Vol, perte ou disparition des biens confiés, sauf vol dans les enceintes des établissements par des préposés ou des tiers avec négligence engageant la responsabilité de l'assuré

- Dommages immatériels consécutifs

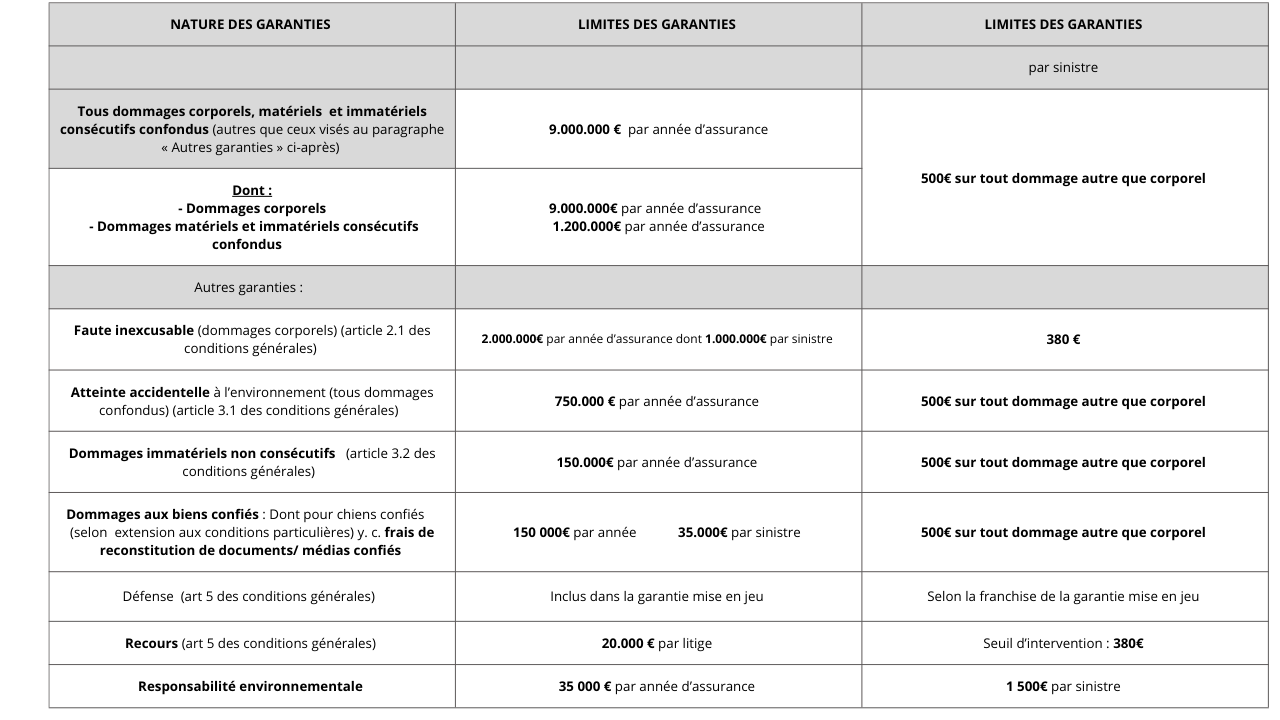

Montant des garanties et franchises

Lorsqu'un même sinistre met en jeu simultanément différentes garanties, l'engagement maximum de l'assureur n'excède pas pour l'ensemble des dommages le plus élevé des montants prévus pour ces garanties, ainsi qu'il est précisé à l'article 6.3 des conditions générales 460653 jointes.

En complément des exclusions prévues par les conditions générales, sont également exclus :

- Dommages liés à des activités soumises à obligation d'assurance ou à des professions réglementées

- Dommages liés aux activités vétérinaires

- Dommages liés à la garde de chiens de catégorie 1 et 2

- Dommages liés aux activités dans les domaines financiers, politiques, pharmaceutiques, médicaux, ingénierie, aéronautique, spatial, nucléaire et armement

- Dommages liés aux activités de conseil en sécurité et prévention

- Dommages liés aux activités de conseil en audit financier, communication, patrimoine, placement et ingénierie financière

- Dommages liés aux activités de construction et rénovation de bâtiments soumises à assurance obligatoire

- Dommages liés à l'utilisation de véhicules terrestres à moteur

Dispositions particulières

Intervention du contrat

Le présent contrat intervient en complément ou à défaut des garanties que l'assuré aurait souscrites par ailleurs.

Étendue géographique

Par dérogation à l'article 6.1 des conditions générales, la garantie s'exerce pour les seuls dommages survenus en France.

Toutefois les garanties sont étendues aux dommages survenus dans le monde entier à l'occasion de voyages de l'assuré ou de ses préposés dans le cadre de stages, missions commerciales ou d'études, simple participation à des foires, expositions, salons, congrès, séminaires ou colloques d'une durée inférieure à trois mois.

Restent en dehors de la garantie les dommages résultant des activités exercées par des établissements ou des installations permanentes situés en dehors de la France.